How the Next Generation of Software Companies Will Create Value

- Jun 1

- 7 min read

The Shift from Product-Centric to Platform-Centric to Intelligence-Centric Businesses

The software industry is entering another once-in-a-generation transformation.

Over the past three decades, software companies have evolved through distinct eras, each defined by a different approach to creating value. Every era produced new market leaders, reshaped customer expectations, and forced established companies to rethink how they compete.

Today, artificial intelligence is accelerating the next wave of change.

Yet the story is much bigger than AI.

Every major technology shift in software eventually becomes a business shift.

The move to cloud changed how software was delivered.

The move to SaaS changed how software was monetized.

The move to platforms changed how companies scaled innovation and ecosystem participation.

AI is following the same pattern.

What appears to be an AI transformation is increasingly becoming a business redesign challenge.

The real story is not the evolution of technology.

The real story is the evolution of how software companies create, deliver, and capture value.

For much of the industry's history, value was created through products.

Then value began to scale through platforms.

Today, value is increasingly being amplified through intelligence.

Understanding this progression is important because it explains why some companies are accelerating while others are struggling to keep pace. More importantly, it provides insight into what may define the next generation of software leaders.

The Three Generations of Software Companies

The evolution of software can be viewed through three distinct generations:

Product-Centric → Platform-Centric → Intelligence-Centric

Each generation builds upon the previous one, but each fundamentally changes how value is created, how companies compete, and how growth is achieved.

Generation One: Product-Centric Companies

For decades, software companies competed through products.

Products were the business.

Products were the strategy.

Products were the primary source of differentiation.

Success was measured through feature leadership, market share, product revenue, and customer adoption.

Value was largely created within the boundaries of the product itself. Innovation focused on delivering more functionality, solving customer problems, and creating better user experiences than competitors.

This model produced some of the most successful software companies in history and remains foundational to the industry today.

However, product-centric businesses eventually encounter natural limits to scale. Growth increasingly depends on adding more features, entering adjacent markets, or acquiring additional products.

As software became more connected and customers demanded greater flexibility, a new model began to emerge.

Generation Two: Platform-Centric Companies

Cloud computing fundamentally changed software economics.

Customers no longer wanted isolated applications. They wanted connected experiences, integrated workflows, extensibility, and continuous innovation.

The most successful organizations responded by shifting their focus from products to platforms.

Instead of asking:

"What functionality should we build?"

They began asking:

"What capabilities should others be able to build upon?"

This seemingly simple shift changed everything.

APIs became strategic assets.

Developer communities became innovation engines.

Partner ecosystems became force multipliers.

Shared services replaced isolated architectures.

Growth was no longer constrained by what a company could build itself. Customers, partners, developers, and ecosystems could now participate in value creation.

The objective shifted from creating value to multiplying value.

Products create value. Platforms multiply value.

This is why platform businesses often outgrow competitors with similar products. Their innovation capacity extends beyond the boundaries of the organization itself.

Yet even platforms are now encountering another transition.

The next generation is not simply about connecting systems.

It is about creating intelligence across them.

Generation Three: Intelligence-Centric Companies

Today, a third generation is emerging.

These organizations are increasingly being built around intelligence rather than software alone.

AI is no longer simply another feature.

It is becoming the interface through which users interact with systems, workflows, and business processes.

The companies leading this generation are not asking:

"How do we add AI to our products?"

They are asking:

"How do we create intelligent systems that continuously generate customer value?"

This is a fundamentally different mindset.

The focus shifts from software functionality to outcome orchestration.

From user workflows to intelligent workflows.

From deterministic systems to adaptive systems.

From executing commands to achieving objectives.

For the first time, software itself is no longer the primary interface.

Users increasingly interact through intent rather than menus, workflows, and screens.

The question is no longer:

"What software should I use?"

The question is becoming:

"What outcome do I want?"

This shift changes how software is discovered, consumed, monetized, and differentiated.

The organizations that recognize this change earliest will have a significant advantage.

However, the companies creating the greatest value from AI are not simply deploying models faster.

They are redesigning experiences, workflows, and business capabilities around intelligence.

The opportunity is not to make existing software slightly smarter.

The opportunity is to rethink how value is delivered in the first place.

That is why the Intelligence-Centric era represents more than a technology transition.

It represents the next business model evolution of the software industry.

Products create value. Platforms multiply value. Intelligence compounds value.

The SaaS Illusion

One of the biggest misconceptions in the software industry is the belief that subscription pricing automatically creates a modern software business.

It does not.

Many organizations have successfully transformed their revenue model.

Far fewer have transformed their business model.

Too many companies completed the commercial transition to SaaS without completing the business transition to platforms.

Cloud hosting is often mistaken for cloud-native architecture.

Subscription pricing is mistaken for platform strategy.

Financial transformation is mistaken for business transformation.

Today, cloud deployment, subscription pricing, cloud-agnostic architectures, and API availability are increasingly becoming table stakes.

Customers expect them.

Investors expect them.

Markets assume them.

They are no longer differentiators.

The next generation of differentiation will come from platforms, ecosystems, exposed business capabilities, and intelligence.

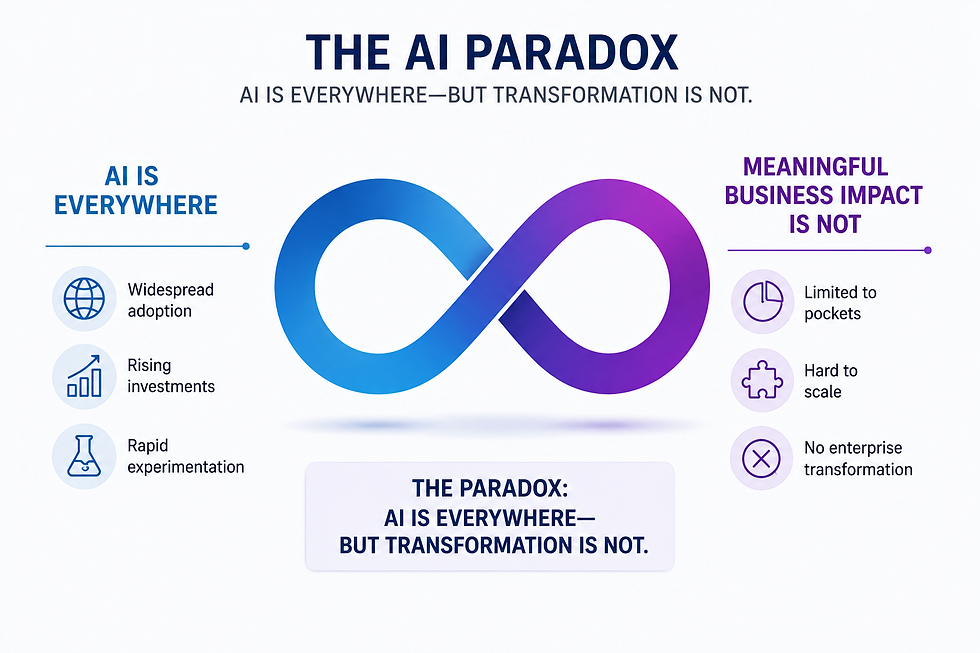

Many organizations believe they are undergoing an AI transformation today.

In reality, many are facing the same challenge they encountered during the transition to SaaS.

Technology adoption often moves faster than business transformation.

Deploying AI is relatively straightforward.

Redesigning products, customer experiences, workflows, monetization models, and value creation mechanisms around AI is considerably harder.

That is where the real transformation occurs.

Cloud is not the destination. Cloud is the foundation.

Three Generations. Three Starting Points.

While the industry is moving toward the same destination, companies are beginning from very different starting points.

For simplicity, software companies can be grouped into three broad categories.

Established software companies largely emerged during the Product-Centric era and have since evolved through cloud, SaaS, and platform transformations. They possess mature product portfolios, deep domain expertise, trusted brands, and decades of customer relationships.

Cloud-native companies were born during the Platform-Centric era. Their businesses were built around SaaS delivery models, API-first architectures, continuous deployment, and platform thinking from the beginning.

AI-native companies represent the newest generation. These organizations are built with intelligence at the core of their products, user experiences, and business models. Rather than treating AI as a feature, they design around intelligent interactions, autonomous workflows, and outcome-driven experiences from day one.

While the distinctions are not absolute, they provide a useful framework for understanding how different organizations are approaching the transition toward the Intelligence-Centric era.

Different Starting Points. One Future.

Although these organizations originate from different generations of software evolution, they are all moving toward the same destination: creating intelligent systems that continuously deliver customer value.

Established software companies possess something that many newer competitors spend years trying to build: deep domain expertise, customer trust, industry knowledge, and real-world business process understanding.

The challenge for these companies is often misunderstood.

The goal is not simply to add AI capabilities to existing products.

The larger opportunity is to leverage decades of accumulated knowledge to create entirely new forms of intelligent value.

Cloud-native companies approach the market differently.

Their businesses were designed around cloud delivery, subscription models, APIs, and ecosystem participation from the beginning. Their advantage lies in speed, architectural simplicity, and platform-oriented thinking.

Many are now extending those platform foundations into intelligence-centric experiences.

AI-native companies represent yet another approach.

Rather than modernizing existing software, they are reimagining software itself.

Their advantage is the ability to design experiences around intent, outcomes, and intelligent orchestration without legacy assumptions.

Their challenge is scale.

Many are still building the customer relationships, ecosystem reach, and industry expertise required to compete with larger software providers.

The Race Is Not What Most People Think

A common assumption is that AI-native companies will automatically dominate the next generation of software.

That assumption may prove overly simplistic.

History suggests that major technology shifts rarely create winners based solely on technology.

The winners are usually those that successfully combine technology with distribution, customer trust, domain expertise, and ecosystem reach.

AI-native companies possess technological advantages.

Established software companies possess domain advantages.

Cloud-native companies possess platform advantages.

The companies that successfully combine these strengths may ultimately define the next generation of market leaders.

The future may not belong to the companies with the best AI.

It may belong to the companies with the deepest business capabilities connected to the most effective AI.

The Real Competitive Advantage

As AI becomes more accessible, intelligence itself will increasingly become commoditized.

Models will improve.

Capabilities will expand.

Costs will decline.

Access will become widespread.

History suggests that sustainable competitive advantage rarely comes from technology alone.

The real differentiators will increasingly be proprietary business capabilities, domain expertise, customer trust, ecosystem participation, unique data assets, workflow ownership, and the ability to convert intelligence into measurable business outcomes.

This is why the next era of software competition will likely be less about who has AI and more about who creates the most value with AI.

Technology may enable the opportunity.

Business redesign captures the value.

Organizations that simply deploy AI may improve efficiency.

Organizations that redesign how value is created, delivered, and captured around intelligence will create entirely new competitive advantages.

The Platform Gap

One of the most significant differences between established software companies and modern platform businesses is platform maturity.

Historically, products protected functionality within product boundaries.

Future growth depends on exposing capabilities beyond those boundaries.

Organizations must increasingly think in terms of reusable business capabilities rather than isolated product functionality.

APIs are no longer integration tools.

They are growth mechanisms.

They enable ecosystems.

They enable automation.

They enable AI.

The future will not be built product by product.

It will be built capability by capability, platform by platform, and intelligence layer by intelligence layer.

Conclusion

The software industry is not simply experiencing an AI transformation.

It is experiencing a business model transformation.

The progression from Products to Platforms to Intelligence represents a fundamental shift in how software companies create, scale, and capture value.

Products defined the first generation.

Platforms defined the second.

Intelligence is defining the third.

But intelligence alone will not determine the winners.

The companies that lead the next decade will be those that successfully combine platform foundations, ecosystem participation, domain expertise, business capabilities, and intelligence-driven experiences to create entirely new forms of customer value.

The first generation of software companies won by building products.

The second generation won by building platforms.

The third generation will win by redesigning how value is created around intelligence.

Products created value. Platforms multiplied value. Intelligence will compound value. Business redesign will unlock that value.

The companies that define the next decade will not necessarily be the ones with the most advanced AI.

They will be the organizations that most effectively combine intelligence, platforms, ecosystems, business capabilities, and customer outcomes into a new model of value creation.

Because the real question is no longer:

"How do we add AI to our products?"

The real question is:

"How do we redesign our business to create intelligent systems that continuously generate value?"

Comments